88YTY News Hub offers a wide range of articles and insights into current events, trends, and much more. Join us for engaging content and in-depth analysis on various topics.

88YTY News Hub Copyright. All rights reserved 2020-2024

Stay updated with the latest trends and news.

Discover how term life insurance can be your unexpected safety net. Protect your loved ones and secure peace of mind today!

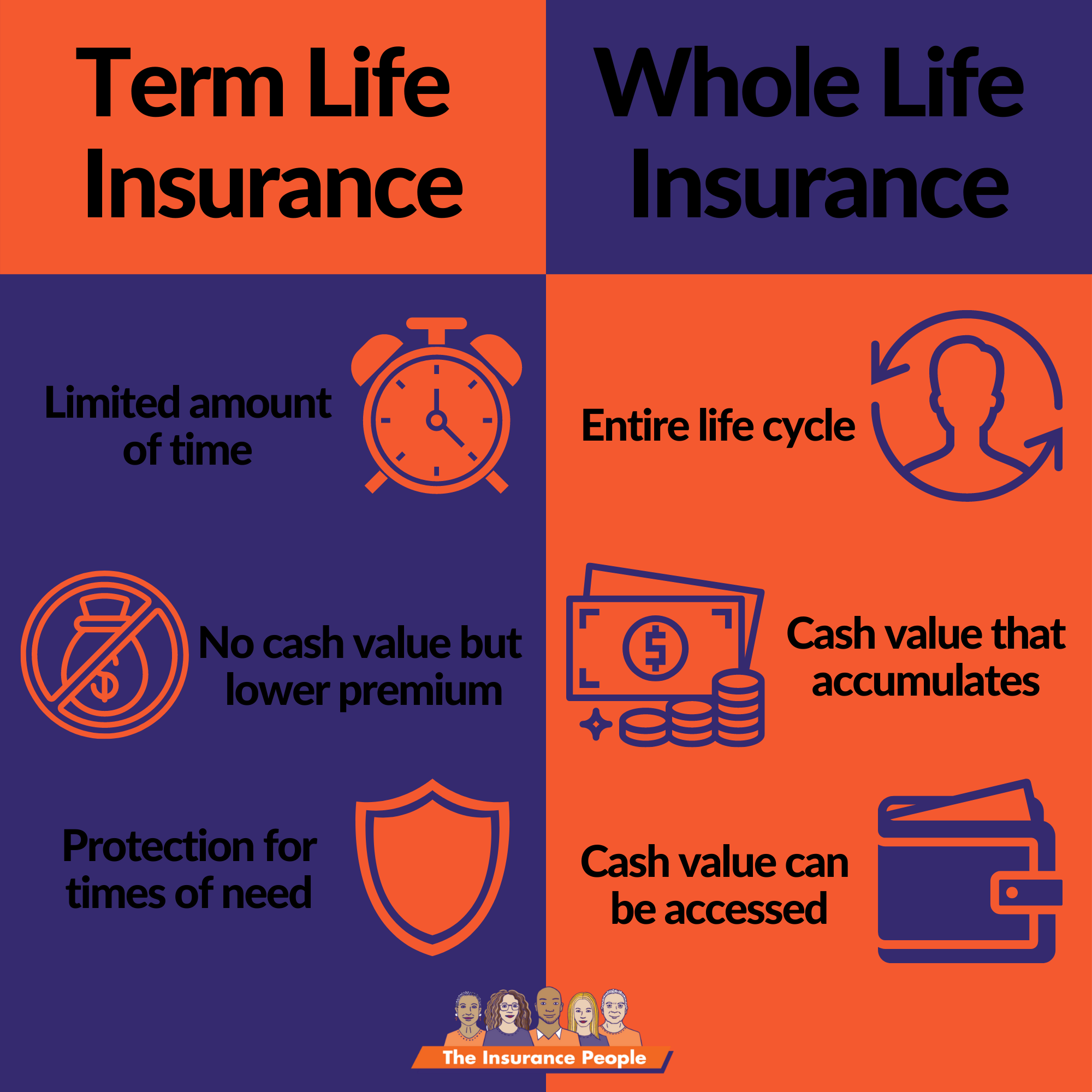

Term Life Insurance is a type of life insurance policy that provides coverage for a specified period, usually ranging from 10 to 30 years. During this term, if the insured individual passes away, the beneficiaries receive a death benefit. This policy is often preferred because it is more affordable compared to whole life insurance, making it accessible for families looking for financial protection without breaking the bank. Term Life Insurance typically does not accumulate cash value, but its straightforward nature and lower premiums make it an appealing choice for individuals seeking peace of mind for their loved ones.

One of the primary reasons why Term Life Insurance is deemed essential is its role in providing financial security in the event of an untimely death. It ensures that dependents are not left in a vulnerable position, covering vital expenses such as mortgage payments, education costs, and daily living expenditures. Without this safety net, families could face significant financial hardships. Additionally, as life circumstances change, the need for coverage can evolve, allowing policyholders to easily convert their term policy to a permanent one for continued protection as they age.

Term life insurance is often misunderstood, leading to several common misconceptions. One prevalent myth is that term life insurance is an investment. Unlike whole life or universal life policies, which can accumulate cash value over time, term life insurance provides pure protection for a specified period, such as 10, 20, or 30 years. When the term ends, there is no payout unless the policyholder passes away during that period. This distinction is crucial as it underscores that term life insurance should be viewed primarily as a safety net rather than an investment vehicle.

Another misconception is that term life insurance is only beneficial for young families. While it's true that many young parents opt for term policies to secure their children's financial future, it's equally valuable for older individuals or those with no dependents. For instance, retirees may use term insurance to cover final expenses or ensure that debts are managed, alleviating the financial burden on loved ones. It's vital to recognize that the versatility of term policies makes them a useful tool for individuals at various life stages.

Choosing the right term life insurance policy is crucial for ensuring your family's financial security in case of an unexpected event. Start by assessing your specific needs, such as the number of dependents, outstanding debts, and future obligations like college tuition. Consider using a needs analysis to help you calculate the appropriate coverage amount. Once you have a clear understanding of your requirements, compare different policies, focusing on factors like premium costs, term lengths, and the reputation of the insurance providers.

Next, it is important to understand the various types of term life insurance policies available. For instance, level term insurance maintains the same premium and coverage amount throughout the term, while decreasing term insurance typically lowers the coverage amount over time, suitable for reducing debts like mortgages. Additionally, determine if you want the flexibility of converting your term policy into a permanent one later. Ultimately, choose a policy that aligns with both your current financial situation and your future goals, ensuring peace of mind for you and your loved ones.