88YTY News Hub offers a wide range of articles and insights into current events, trends, and much more. Join us for engaging content and in-depth analysis on various topics.

88YTY News Hub Copyright. All rights reserved 2020-2024

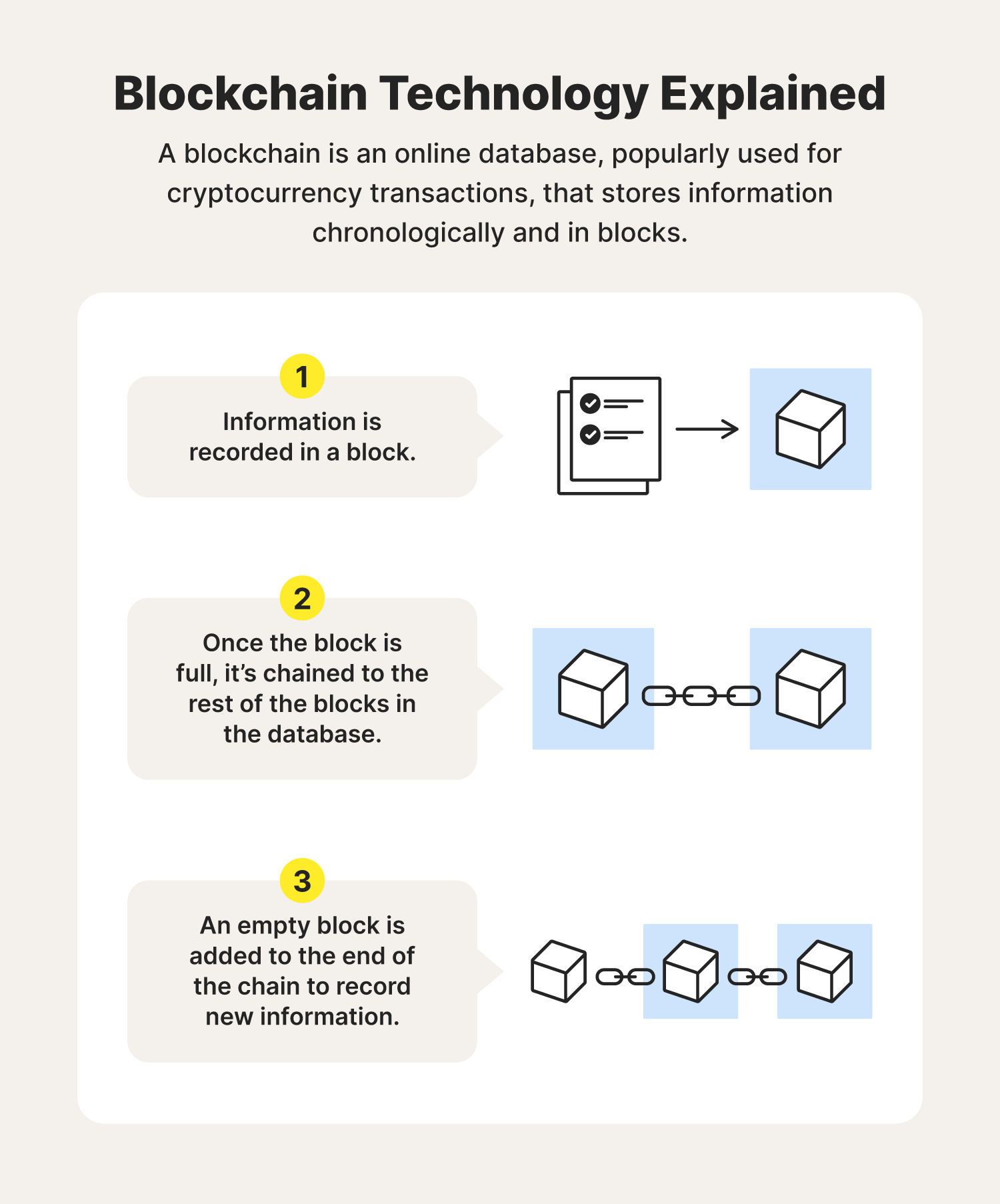

Stay updated with the latest trends and news.

Discover how blockchain is shaping the future economy and why it’s the unseen backbone driving innovation and growth. Don't miss out!

The integration of blockchain technology in supply chain management is transforming traditional processes by enhancing transparency and accountability. With blockchain, every transaction is recorded on a decentralized ledger, allowing all stakeholders to access real-time information about the flow of goods. This increased visibility helps to reduce fraud and errors, as well as improving compliance with regulations. Companies can trace the origins of products, ensuring quality and authenticity, which is especially crucial in industries like food and pharmaceuticals.

In addition to transparency, blockchain is streamlining operations through automated processes like smart contracts. These self-executing contracts automatically enforce the terms of an agreement when certain conditions are met, reducing the need for intermediaries and minimizing delays. As a result, organizations can experience enhanced efficiency and lower operational costs. The shift towards a blockchain-enabled supply chain not only boosts productivity but also fosters strong relationships amongst all participants, cultivating a more resilient and agile supply chain ecosystem.

Smart contracts represent a revolutionary step in the evolution of automated agreements, leveraging blockchain technology to provide secure, transparent, and self-executing contracts without the need for intermediaries. These digital contracts are programmed to automatically enforce and execute the terms of an agreement when predetermined conditions are met, thereby reducing the potential for disputes and enhancing trust among parties. By eliminating middlemen such as lawyers or notaries, smart contracts not only decrease costs but also streamline processes, making them an attractive option for various industries, including real estate, finance, and supply chain management.

As we move toward a more digital and interconnected world, the adoption of smart contracts is expected to grow significantly. Their potential applications range from automating complex transactions in finance to ensuring the authenticity of products in supply chains. To fully understand their impact, consider the following key benefits:

Blockchain technology has been surrounded by numerous myths that often cloud its true potential. One of the most common misconceptions is that blockchain is synonymous with Bitcoin. While Bitcoin is indeed built on blockchain technology, blockchain itself is a versatile tool that can be used in various applications beyond cryptocurrencies. Understanding blockchain as a broader technology allows businesses and individuals to leverage its benefits in sectors such as supply chain management, healthcare, and even voting systems.

Another prevalent myth is that blockchain is completely anonymous. In reality, while user identities can be obscured, all transactions are recorded on a public ledger that anyone can access. This transparency provides a level of accountability that isn't always present in traditional systems. Rather than being entirely anonymous, blockchain technology offers pseudonymity, making it crucial for users to understand how their data can be tracked and verified.